State of Delaware Drinking Water Revolving Loan Fund FY22-FY23

Financial Statement Audit – Fiscal Years Ended June 30, 2022 and 2023

Report Summary

Background

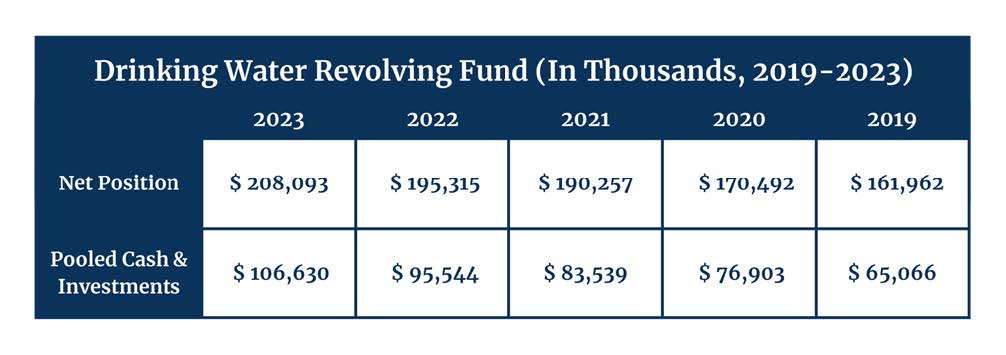

The Drinking Water State Revolving Fund (DWSRF) Fund was established in 1996 and provides financial assistance to eligible public water systems in Delaware for the planning, design, and construction of drinking water facilities, as well as loans for land acquisition for source water protection purposes.

The Fund is funded through federal grants as established under the Federal Safe Drinking Water Act and the Capitalization Grants for the Drinking Water State Revolving Loan Fund. The Safe Water Drinking Act requires the State of Delaware (the State) to provide matching funds equal to 20% of federal funds received. The Delaware Department of Natural Resources and Environmental Control (DNREC) and the State of Delaware Department of Health and Social Services (DHSS) administers the fund.

During fiscal year ended June 30, 2023, the Fund received additional grants (Emerging Contaminants Grant, Lead Service Line Grant, and General Supplement Grant) funded by the Infrastructure Investment and Jobs Act (IIJA) which provides funds for the DWSRF program. The additional grants are to provide low interest financing to numerous subrecipients for costs associated with the planning, design, and construction of eligible water quality improvement and protection projects. EPA authorized the Fund to issue subsidization through principal forgiveness loans with a policy to maintain an allowance equal to the amount of disbursement until the last disbursement is made. The State is not required to match funds for the Emerging Contaminants or Lead Service Line Grants, however, is required to provide matching funds equal to 10% of the General Supplemental Grant.

This engagement was conducted in accordance with 29 Del. C. §2906.

Key Information and Findings

This audit contains an unmodified opinion on the financial statements. An unmodified opinion is sometimes referred to as a “clean” opinion, in which the auditor expresses an opinion that the financial statements are presented fairly, in all material respects, an entity’s financial position, results of operations, and cash flows in conformity with accounting principles generally accepted in the United States of America. There were no findings required to be reported under Government Auditing Standards.