Long Term Care Facilities FY22

Examinations – Fiscal Year Ended June 30, 2022

Sign Up For Our Audit Reports Email Distribution List

Executive Summary

Background

An examination of 14 Long-Term Care Facility fiscal records of the Delaware Department of Health and Social Services, Division of Medicaid and Medical Assistance, Medicaid Long-Term Care Facilities’ Statement of Reimbursement Costs for Skilled and Intermediate Care Nursing Facilities – Title XIX and Nursing Wage Survey (cost report and nursing wage survey, respectively) for fiscal year ended June 30, 2022.

The State Auditor is authorized under 29 Del. C., §2906 to conduct audits of all financial transactions of all state agencies.

These engagements were conducted in accordance with federal requirements (42 CFR 447.253 and 483 Subpart B) and state requirements (Title XIX Delaware Medicaid State Plan, Attachment 4.19D) (criteria), as applicable to the Long-Term Care Facility fiscal records. The criteria were used to prepare the Schedule of Adjustments to the Trial Balance, Patient Days, and Nursing Wage Survey for fiscal year ended June 30, 2022, found in the reports.

Key Information and Findings

All of the fourteen (14) long-term care facilities examined received unmodified opinions and complied, in all material respects, with the criteria mentioned.

All facilities audited did have adjustments or findings in the reports. Under Governmental Auditing Standards, the adjustments and findings do not materially impact the examination. However, the findings are included to alert the readers of the reports with the comments made during the examination.

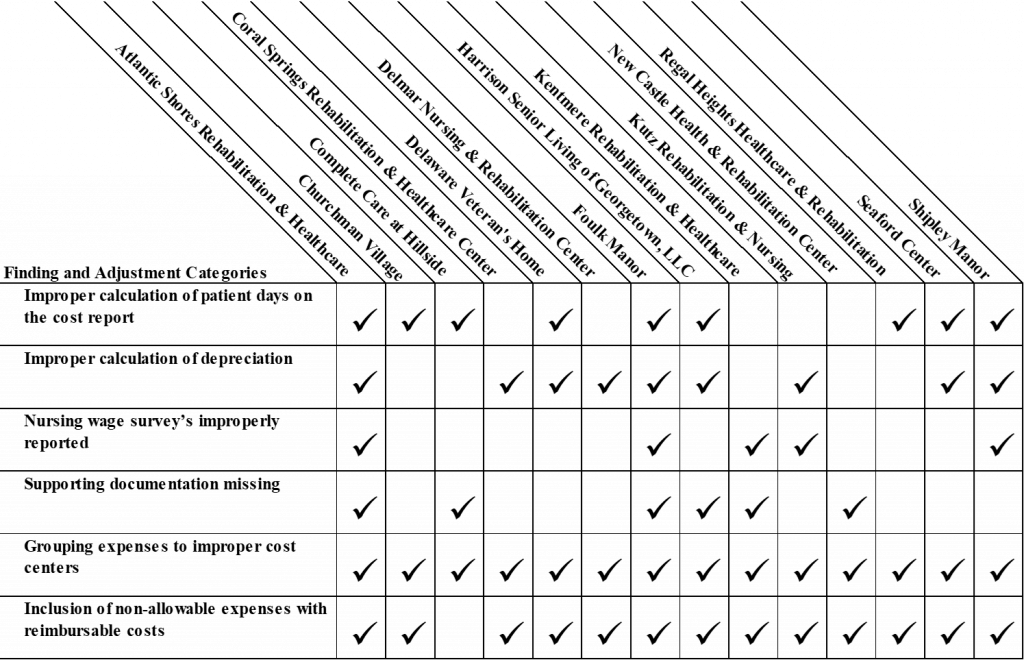

Common findings and adjustments included:

- Improper calculation of patient days on the cost report

- Improper calculation of depreciation

- Nursing wage survey’s improperly reported

- Supporting documentation missing

- Grouping expenses to improper cost centers

- Inclusion of non-allowable expenses with reimbursable cost

For the findings, two of the 14 facilities’ management did not provide a response acknowledging the issue or the plan to address the findings found during the audit.

The large volume of non-material audit findings (an average of 8, with a high of 14 per facility) is a strong indicator of deteriorating or weak internal controls within these long-term care facilities (LTCFs). The findings, though individually non-material, risk that many small, non-material errors can aggregate to cross the threshold for materiality, resulting in a modified opinion.

While the audits issued an unmodified opinion (meaning no material misstatement), the numerous findings point to a breakdown in the day-to-day systems and procedures designed to prevent and detect errors. The sheer number of issues means the facilities are relying on external auditors to catch errors, a sign that the internal system is failing.

Full Audit Reports

- Atlantic Shores Rehabilitation and Health Center

- Churchman Village

- Complete Care at Hillside

- Coral Springs Rehabilitation and Healthcare Center

- Delaware Veterans Home

- Delmar Nursing and Rehabilitation Center

- Foulk Manor Long Term Care Facility

- Harrison Senior Living of Georgetown

- Kentmere Rehabilitation and Healthcare

- Kutz Rehabilitation and Nursing

- New Castle Health and Rehabilitation Center

- Regal Heights Healthcare and Rehabilitation Center

- Seaford Center

- Shipley Manor