Distressed Cemetery Fund 2024

Examination – Fiscal Year Ended June 30, 2024

Sign Up For Our Audit Reports Email Distribution List

Report Summary

Background

The Office of Auditor of Accounts (AOA) performed an examination of the Schedule of Cash Receipts and Cash Disbursements of the State of Delaware Distressed Cemetery Fund (Fund) for the fiscal year ended June 30, 2024 to determine whether it is in accordance with the criteria set forth in the Delaware Code and the State of Delaware Budget and Accounting Policy Manual (BAM).

The objectives of the examination engagement included the following:

- Determine if registration fees (revenues) are accurately applied to an account in accordance with 29 Del. C. 7906A

- Determine if death certificate fees (revenues) are accurately applied to an account in accordance with 29 Del. C. 7907A (a)

- Determine if DCF receives and forwards complaints from any person relating to a Delaware cemetery to appropriate agencies of the State in accordance with 29 Del. C. 7904A (8)

- Determine if the DCF Board:

- Resolved that cemeteries of applicants are considered ‘distressed’ in accordance with 29 Del. C. 7904A (5), and either authorized or rejected work to be performed at distressed cemeteries in accordance with 29 Del. C. 7904A (6).

- Authorized payment to distressed cemeteries from the Fund in accordance with 29 Del. C. 7904(6).

- Obtained a thorough accounting of each recipient’s use of money from the Fund in accordance with 29 Del. C. 7904A (7).

- Is keeping records related to meetings of the Board per 29 Del. C. 7904A (1) (3).

- Confirm the existence of department policies and procedures and ensure that they are properly managed and maintained. In addition, evaluate the effectiveness of policies and procedures in fulfilling goals and strategic objectives.

The audit was performed according to AOA’s authority as set forth in 29 Del. C. §7907A. This law previously mandated an audit of the Distressed Cemetery Fund annually. Effective August 21, 2025, it now mandates an audit at least once every five years.

Key Information & Findings

During FY24:

- A total of 267 cemeteries were registered with the fund through June 30, 2024.

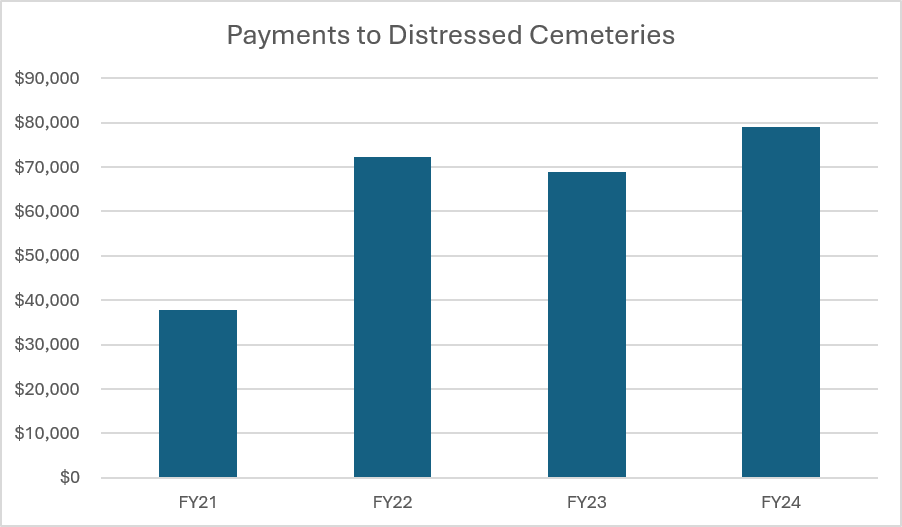

- A total of six cemeteries were approved to received distressed cemetery funds totaling $78,993.00 in awards for fiscal year ending June 30, 2024.

- A total of $21,007.00 was reverted to the general fund for fiscal year ending June 30, 2024.

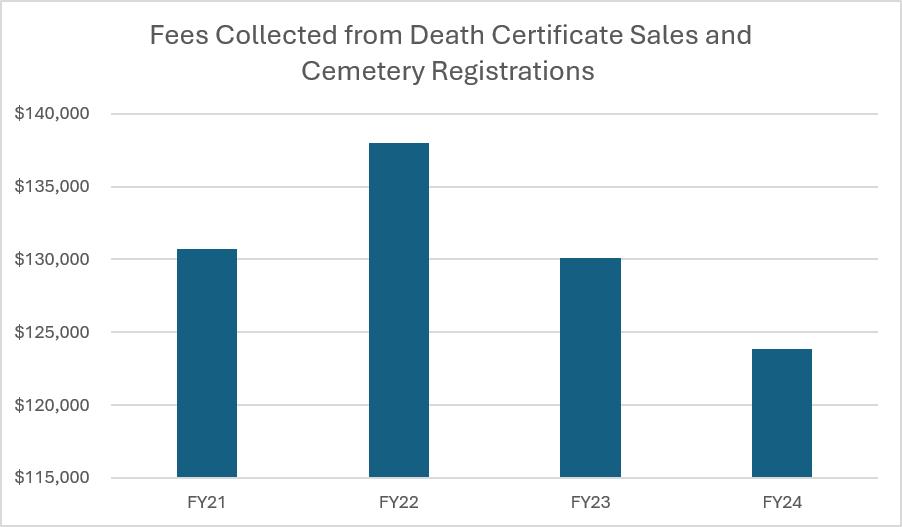

Fees collected from death certificate sales and cemetery registration fees for fiscal year ending June 30, 2024, totaled $123,831.08

There were two instances of significant deficiencies in internal controls. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness yet important enough to merit attention by those charged with governance.

- Fractional Transactions: AOA observed instances in which the full death certificate fee amount was not accounted for properly.

- Cash Receipts Supporting Documentation: The supporting documentation for allocation of death certificate fees to the Fund were incomplete in several of the sampled deposits due to of the insufficient document retention guidance.